Easier to read and understand, our 2024-25 Federal Budget Summary wraps up the key changes and introductions that are likely to impact the property market.

Growth Expected

Economic growth is forecast at 2% next year and 2.25% in 2025-26

Inflation to Fall

The treasury expects inflation to fall to 2.75% by June 2025 (a more optimistic view than what the RBA has forecast).

Employment to Slow

Employment growth is forecast to slow from 2.25% this year to 0.75% in 2024-25, with unemployment rising to 4.5%.

Increased Borrowing Power

Boosts from Tax Cuts

Homebuyers will be able to borrow tens of thousands more next financial year due to tax cuts aimed at lowering the cost of living.

Higher Take-Home Pay

Adjustments to tax rates will increase most taxpayer’s take home, enhancing their ability to borrow for a home.

Auction Advantage

This increase in savings could make a significant difference during home purchases, potentially being the deciding factor in competitive bids.

Advantage for Dual Income Homes and First Home Buyers

Households with dual incomes will see a more substantial impact, potentially doubling the borrowing capacity increase.

Higher interest rates have constrained borrowing capacities for first-home buyers in the past, making the tax cuts particularly beneficial. Those buying affordable properties will benefit the most from the increased borrowing capacity.

Tax Cut Timing

Banks may take a month or so to update their calculators to reflect tax cuts, but brokers can manually adjust calculations sooner – allowing home buyers to take advantage of their additional take home pay sooner.

How will the 24-25 Federal Budget impact your property goals?

Wondering how this will impact your property goals? Whether you’re looking to buy, sell or invest, our team is here to help. Get in touch todayto see how we can help make your property goals a reality.

We often associate Spring with renewal, fresh beginnings and cleaning and decluttering at home, but what about your finances? As the real estate market ramps up, there’s no better time to embark on a financial spring clean, especially if you’re in the market to buy.

A clean financial state not only improves your chances of securing a mortgage, but also sets you up for a more stable financial future – so let’s look at some of the ways you can tidy up your finances:

Refresh (or set) your budget

It’s easy to set and forget a budget – or not set one at all.

Dinners out, streaming subscriptions, coffees and impulse shopping can quickly add up. When applying for a home loan, this spending is what lenders tend to scrutinise – so why not clean this spending up now. Have a look at our previous article, How your Daily Spending is Impacting Your Borrowing Power for some tips.

Netflix, Disney+, Kayo, One Pass, Amazon Prime, gym memberships – monthly subscriptions can quickly add up, and for many of us they are often left unused.

Why not look at all of the weekly/monthly/annual subscriptions you have and then decide what can stay, go or swap for a cheaper (or free) option. You may find that you end up saving hundreds each month on subscriptions you simply don’t need.

Reassess your financial goals

Do you have financial goals? If so, when’s the last time you checked in with them? If not, why not start now? By setting a goal, you have something to work towards and be aware of. Some great financial goals to get you started include:

Sticking to a budget

Increasing your income

Saving for a house deposit

Putting money towards retirement

Breaking the paycheck-to-paycheck cycle

Re-think your spending

Have you ever stopped to look at what you’re spending, where you’re spending it and how much you’re spending?

You might be surprised to find that those small regular expenses quickly add up and impact your saving goals – and these expenses are often what lenders scrutinise.

Have a look at your income and expenses as a whole and see where there’s room to reduce expenses, increase savings or change your spending habits to be more in line with your financial goals.

Take inventory of debts

What money comes out of your account each month? Could you consolidate or remove some of those debts? Paying off your various debts via a single loan with a competitive interest rate not only helps you save money, it also leaves you with one simple payment date each month. This, in turn, may help reduce financial stress.

Debt consolidation is something we can help you with. Want to get started? Contact us today.

Prepare for the unexpected

Accidents happen, illness occurs, appliances break and all when you least expect it. An emergency fund can be the difference between an event being a crisis or an inconvenience and it’s so important that you make sure your emergency fund is fully funded and up to date.

Three to six months of essential expenses saved in a separate bank account is the general rule of thumb for an emergency fund, but even a small amount can make a big difference. If you don’t have the funds to transfer right away, why not start small and make a plan to build that fund with weekly or monthly deposits.

Make sure you’re getting the best deal

Are you paying too much for your insurance or household bills? Whilst many companies offer incredible deals to sign up with them, very few companies offer great deals or incentives for existing customers.

Many of us are too busy (or just don’t think about it) to check whether or not we’re getting the best deal. This typically means that we’re spending extra money each month for no reason.

Not sure where to start? We recommend comparing rates and deals on the below:

Utilities (gas, electricity, water)

Insurances (home, health, car)

Internet and Phone Plans

Also be sure to let your current provider know that you’re looking for a better deal. More often than not, they’ll offer you a discount or match the price to retain your business.

Ready to get started?

By reviewing your credit, improving your financial health and rethinking your spending, you’ll be well on your way to achieving your homeownership goals.

Need some help to get started? Contact us today and let’s get ready to welcome the summer in your new home.

There are many different ways to purchase property – and one of those ways actually involves committing to purchasing a property that doesn’t yet exist.

Buying real estate ‘off the plan’ means committing to purchasing a property that is still in the pre-construction or early construction phase, often long before a building or development project is completed. Many home owners and investors see buying off the plan as a good way to purchase a brand new property, however, just as with any investment, there are pros and cons to consider – so let’s have a look at them.

The benefits of purchasing property off the plan

Lower Purchase Price One of the main attractions of buying off the plan is the potential to secure the property at a lower price than it would be once construction is finished. Developers often offer discounts and incentives to early buyers which can result in significant savings.

Potential Capital Appreciation In a rising property marketing, purchasing off the plan can be a smart investment strategy. As property values will likely increase during the construction period, buyers may benefit from capital appreciation ever before they’ve settled on the property.

Customisation Opportunities This benefit particularly applies to home owners, but also provides investors with opportunities to boost their potential rental income. Purchasing off the plan often gives you the chance to customise certain aspects of the property, including selecting finishes, materials or layout preferences to suit their specific needs and tastes.

Delayed Payment When purchasing off the plan, buyers typically pay a deposit upfront and the rest of the purchase price upon completion. This extended settlement period provides you with extra time to save or secure finance.

Stamp Duty Savings As Stamp Duty is only payable on the land for off the plan purchases, you could be savings thousands of dollars on your purchase.

Deposit Options Whilst most buyers pay cash to secure their deposit, purchasing off the plan provides you with other more flexible deposit options to consider, including Bank Guarantees and Deposit Bonds. It’s always best to check with your property consultant as to what method of payment the develop is happy to accept.

Tax Advantages Being a new property, investors can claim depreciation which is a major tax incentive. This helps to reduce the ongoing costs of holding the property, allowing you to build a larger portfolio.

The disadvantages of purchasing property off the plan

Uncertainty One of the things that potentially buyers are often afraid of is the uncertainty of buying off the plan. As the property is yet to be constructed, buyers have to rely on floor plans, artist impressions and development promises as they’re not yet able to see the final product.

Construction Delays and Risks Construction projects can face unexpected delays due to various factors, such as weather, planning permits, development applications or financial issues. These delays may result in buyers having to wait longer for the property’s construction, impacting their plans.

Market Fluctuations Whilst a rising property market can bring capital appreciation, a declining market can have the opposite effect. If property values drop during the construction period, buyers may find themselves with a property worth less than they originally paid.

Changes in Financial Circumstances A buyer’s financial situation may change between time of purchase and completion, as well as general economic circumstances. This can make it harder to secure financing or meet the financial requirements during settlement.

How can you mitigate risk and increase your chances of securing finance for your off the plan purchase?

As mentioned above, economic or personal circumstances may change between the time of purchase and completion, however, below is what we always recommend our clients do to ensure they can reduce risk and have the best chance of securing finance for their property:

Increase your savings This will help to cover any unlikely shortfalls

Do not apply for any lines of credit during this time Don’t be tempted by credit card offers and avoid signing up for any additional lines of credit whilst waiting for your property to be completed. This could impact your borrowing capacity or credit rating.

Ensure all commitments are paid on time and up to date No lender likes to see late or outstanding payments, so make sure you’re paying all commitments on time.

Don’t change employment Some lenders can have issues with short term employment so it’s important that you chat to us should your employment change.

Maintain or reduce your living expenses Increasing your lifestyle costs may reduce your borrowing capacity so it’s important to keep an eye on your budget.

What should you consider when purchasing off the plan?

We’ve talked about the pros and cons, but what things do you need to consider when purchasing off the plan?

Research the developer You want to make sure that you thoroughly research the developer’s reputation, track record and completed projects prior to committing to an off-the-plan purchase as this will give you an idea of their creditability and their quality of work.

Understand the Contract Ensure you carefully review the purchase contract with the help of a legal professional. Pay close attention to clauses regarding potential changes in the property’s design, timeline and provisions for compensation in case of construction delays.

Finances It’s important that you know what you assess your financial situation and consider the risks associated with the investment before committing. When working with Sanford Finance, we’ll sit down to work out your goals, discuss potential risks and action plans and discuss contingency plans in case of unforeseen circumstances to ensure you’re not jumping into anything you’re not prepared for.

Location and Market Analysis Think about the location of the development and its potential for future growth. Consider things like the demand for similar properties in the area and evaluate the long term investment potential for the property.

What finance options are available during the construction phase?

Purchasing a property off the plan can be quite stressful and challenge even the best laid plans, however, our construction loans take a lot of stress out of the equation.

A construction loan most commonly has a progressive drawdown where you receive instalments of the loan at various stages of construction, rather than receive it all at once at the start.

This means that you generally only pay interest on the amount that is drawn down, as opposed to the entire loan amount.

A number of lenders also offer construction loans that are interest-only during the construction period, later reverting to a standard principal and interest loan once the build is complete.

Construction Loan Case Study:

Craig and Belinda are purchasing land for $300,000 in Adelaide and building a new home for $400,000 for a total value of $700,000. They are borrowing 95% or $665,000. Assuming an interest rate of 5.95%, the repayments required by Craig and Belinda during the build phase will look like this:

Current Loan

Current Loan

Current Loan

Min. Monthly Repayment Required

Land Loan

Nil

$265,000

$1,314 IO

Deposit 5%

$20,000

$285,000

$1,413 IO

Base 15%

$60,000

$345,000

$1,710 IO

Frame 20%

$80,000

$425,000

$2,107 IO

Enclosed 25%

$100,000

$525,000

$2,603 IO

Fixing 20%

$80,000

$605,000

$2,999 IO

Practical Completion 15%

$60,000

$665,000

$3,966 P&I

Totals

$400,000

$665,000

IO = Interest Only P&I = Principal and Interest

In the above table we can see that the repayments steadily increase over time and are interest-only during the build phase. Once the final payment is made, a construction loan will generally convert to Principal and Interest repayments.

How do you get started?

Buying off the plan can be exciting and nerve wracking all at the same time, but we’re here to help. We’ve helped many clients secure their dream property or investment property off the plan and know what you should be looking for, what lenders are looking for and are here to help you navigate the off-the-plan market more confidently.

The decision to buy or sell property is always a tricky one, as it’s a significant financial step that involves careful consideration of various factors – including market conditions.

Whilst it’s important to know that real estate markets can be unpredictable, understanding the key indicators can help you to make an informed decision. So, let’s look at the factors influencing the Australian property market.

Low Listing Numbers = Increased Competition for Buyers

With decade-low listing numbers, there’s not a lot of competition in the market for vendors – but competition is fierce for buyers as they battle it out to secure a property. This is one of the reasons that selling conditions have strengthened, as evidenced by above average clearance rates, faster selling time and less negotiation.

The total number of homes listed for sale across Australia is currently 28% below usual (as reported by CoreLogic). When these volumes are low, selling conditions strengthen, meaning that potential vendors thinking about selling may jump in now rather than waiting until the traditional spring period where activity surges and there’s a spike in competition.

Rising Prices

Home values for Sydney, Melbourne, Brisbane and Perth all recorded an increase in housing values from the lows recorded in February. A mid-month update based on CoreLogic Australia’s daily Home Value Index showed the upswing gathering momentum, especially in cities such as Brisbane where the index is up 1.0% over the past four weeks whilst the Sydney property market still remains the strongest.. Considering housing affordability measures remain stretched such a strong rate of growth is surprising, with many experts predicting that this price rise will not be sustainable in the long term.

Low Supply vs High Demand

As mentioned above, decade-low listing numbers and high demand has lead to fierce competition between buyers – as seen in auction clearance rates that have been holding at 70% or higher in recent weeks.

In a time where the market traditionally tends to cool off, the stats suggest that, if anything, the market is gathering momentum instead of slowing down. Strong clearance rates as well as faster selling times and reduced discounting rates indicate that it’s definitely a vendor’s market.

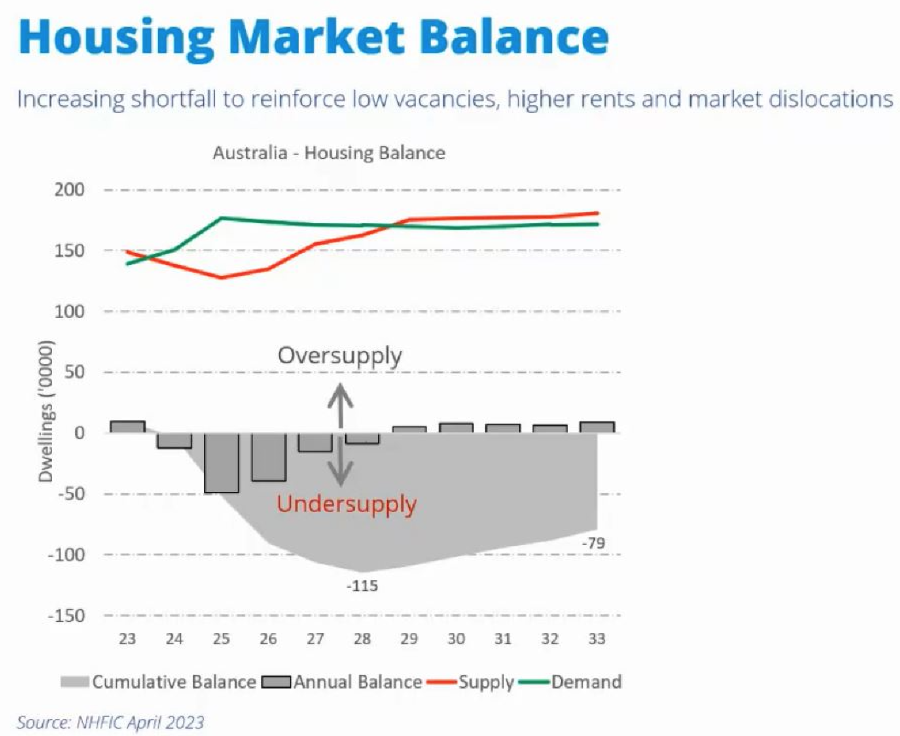

Recent data from the National Housing Finance and Investment Corporation shows a 115,000 dwelling undersupply for 2028.

Interest Rates Continue to Rise

The biggest challenge for potential and current property owners? Interest rates. With interest rates continuing to rise, demonstrating an ability to service a loan remains one of the biggest challenges for prospective buyers to face.

Interest rates are high, but assessment levels are three percentage points higher again – making it even harder for buyers to enter the market or secure their dream property.

Economic Uncertainty

In addition to rising interest rates, we’re also in the midst of a cost of living crisis where consumer confidence is low.

Should RBA cut interest rates, there’s a good change we would see a pick-up in both buyer and seller activity. It’s also highly likely that lower interest rates would be the catalyst for a further uptick in housing values, however, we’re not expecting a rate cut anytime soon and there’s speculation that rates may continue to rise this year.

Economists are split on their forecasts with predictions for further rate hikes, stability and some cuts later this year – all contributing to uncertainty and low consumer confidence levels.

A Helping Hand

Government policies and regulations play a crucial role in shaping the property market. Policies related to taxation, lending practices, and housing affordability can have both direct and indirect effects on the market.

At the moment, first home buyers in particular have a wide variety of grants, concessions and schemes available to them (outlined in our First Home Buyer Update here) that could make purchasing a property easier and more affordable.

Migration Predicted to Recover

With net overseas migration set to fully recover to pre-pandemic levels there will be more pressure on the housing market than we’ve seen in recent years.

With the return of international students and the surge in migration, it is estimated that an extra half a million people will be looking for somewhere to live in Australia in the next two years.

Low vacancy rates bringing investors into the market

We are experiencing a rental crisis across the country, with historically low vacancy rates encouraging more investors into the market. Unfortunately for investors, rising interest rates and property prices have made this challenging – as well as rising building costs making it harder for investors and developers to buy and renovate or rebuild.

Is now the right time to buy or sell?

In short? Maybe. Unfortunately it’s not a one size fits all answer.

Ultimately, making an informed choice that aligns with your own circumstances and long term goals is key when navigating the property market.

Luckily, we’re here to help. We’ll sit down to work out what your goals are, what your property budget may be and how we can help you secure a property. Contact us today to get started!

First Home Owner Update – What’s Changing on July 1

From July 1, 2023, the New South Wales Australian Labor Party (ALP) will implement changes that will impact the way many first home owners purchase property. To make the transition easier, we’re going to run you through some of these changes and how they could impact you.

Stamp Duty Concessions

The ALP will introduce changes to stamp duty for first home buyers. Currently, first home buyers are exempt from paying stamp duty on properties valued up to $650,000, and receive a concession on properties valued between $650,000 and $800,000.

From July 1, 2023, these thresholds will be increased to $800,000 and $1 million respectively, providing even more support for those looking to purchase their first home.

Changes to the First Home Owner Grant

On July 1, the First Home Owner Grant will be increased from $10,000 to $25,000 for eligible first home buyers purchasing a newly constructed home or an off-the-plan property. This grant will be available for properties valued up to $1 million, and will provide a significant boost to those trying to get into the property market.

Removal of the Home Buyers Buyer Choice Scheme

Under the newly elected Minns Labor Government, the NSW Government will now abolish the First Home Buyer Choice scheme, reverting to the new stamp duty concessions as mentioned above.

Over 4,200 First Home Buyers had selected the First Home Buyer Choice options since it was rolled out in November 2022.

For those First Home Buyers who had already selected the property tax option there will be a grace period and it would be unlikely that the new NSW government would reverse any existing arrangements. We will continue to monitor this and keep you updated.

First Home Guarantee Eligibility to Expand

Previously, the First Home Guarantee and Regional First Home Guarantee Schemes were restricted to married and single people, as well as those in defacto relationship who were also Australian citizens at the time of application.

From July 1 this year, the Home Guarantee Scheme will expand, allowing permanent residents to access the scheme as well as allowing friends, siblings and other family members to jointly apply for the guarantees. These schemes will also be available to non-first home buyers who have not owned a property in the past 10 years.

For both of these schemes, the federal government acts as a guarantor on up to 15% of the loan. This enables eligible buyers to purchase a home with as little as a 5 percent deposit, eliminating the need for lender’s mortgage insurance.

Family Home Guarantee Changes

The criteria for Family Home Guarantee applications will also be expanded beyond just single natural or adoptive parents with dependents. This means that the guarantee will be available to eligible borrowers who are single legal guardians of children, such as aunts, uncles and grandparents.

Under the Family Home Guarantee, the federal government acts as a guarantor on up to 18% of the loan. This enables eligible buyers to purchase a home with as little as a 2 percent deposit, eliminating the need for lender’s mortgage insurance.

The availability of this guarantee will also expand to include permanent residents in addition to Australian citizens.

How do I know if I’m eligible?

Our team will help you identify which Guarantees could be applicable to you under the Home Guarantee Scheme (HGS)

We’ll help you find the right path to owning your own home and will be with you every step of the way. To get started, simply get in touch to organise a call or meeting.