Changes to NSW Rental Laws in 2025: What Landlords and Tenants Need to Know

If you’re a tenant or landlord in NSW, you may already know that big changes are coming to rental laws in 2025 – and some were already put in place late last year. These reforms aim to make renting fairer, providing tenants with more security whilst providing landlords with clear guidelines to follow.

In October 2024, the NSW Parliament passed the Residential Tenancies Amendment Act 2024, which introduced significant updates to how rental agreements will work – but we’ve done the hard work of reading through the act and picked out the bits you need to know:

What has already changed (from October 31, 2024)

- No more extra fees at the start of a tenancy

Tenants can no longer be charged fees for background checks or preparing tenancy agreements. - Rent increases limited to once per year

Previously this rule only applied to periodic leases and fixed-term leases longer than two years. Now all rental agreements, regardless of length or type, can only have one rent increase per year.

What changes will be made to rental laws in 2025

- Ending ‘no grounds’ evictions

Landlords will now require a valid reason to terminate a lease, whether it’s a periodic or fixed term. Landlords must provide evidence with termination notices to support their claims, with penalties applying if the given reason is not genuine.Acceptable reasons include:

- The property is being sold

- Major repairs or renovations require the home to be vacant

- The landlord or their family intends to move in

- The tenant has breached their lease agreement

- More notice required for fixed-term leases ending

Tenants will now receive more time to find a new home at the end of their lease. Minimum required notice periods are now:- 60 days notice for leases of six months or less

- 90 days notice for leases longer than six months

- Easier rules for keeping pets

Tenants will have a clearer and fairer process for keeping pets in rental properties, with key changes including:- Tenants can apply to keep a pet and landlords can only refuse for specific reasons

- Landlords must respond to pet requests within 21 days, or a pet is automatically approved

- Landlords cannot increase rent or require extra bond as a condition of allowing a pet

- Strata by-laws that ban all pets will now be invalid under the new rules

- Free and convenient ways to pay rent

Landlords and agents must offer tenants at least one electronic payment method, such as bank transfer or BPAY, without extra fees. Tenants cannot be forced to use a specific payment service or app that charges fees unless they agree to it.

- Water efficiency requirements (from 23 March 2025)

If landlords want to charge tenants for water usage, properties must meet stricter water efficiency standards. The main change is that toilets must be dual flush with at least a 3-star WELS rating, in addition to existing water-saving requirements

How will these changes be enforced?

To ensure compliance to the new laws, NSW Fair Trading has set up a new Rental Taskforce with dedicated inspectors and compliance officers. Any landlord who fails to follow the new laws can be reported and may face penalties.

How can I keep up with changes to rental laws?

With rental laws evolving, it’s important you keep up with the changes – particularly if you are a landlord. The easiest way is to sign up for the NSW Fair Trading Property Matters Newsletter or visiting the Rental Commissioner Website.

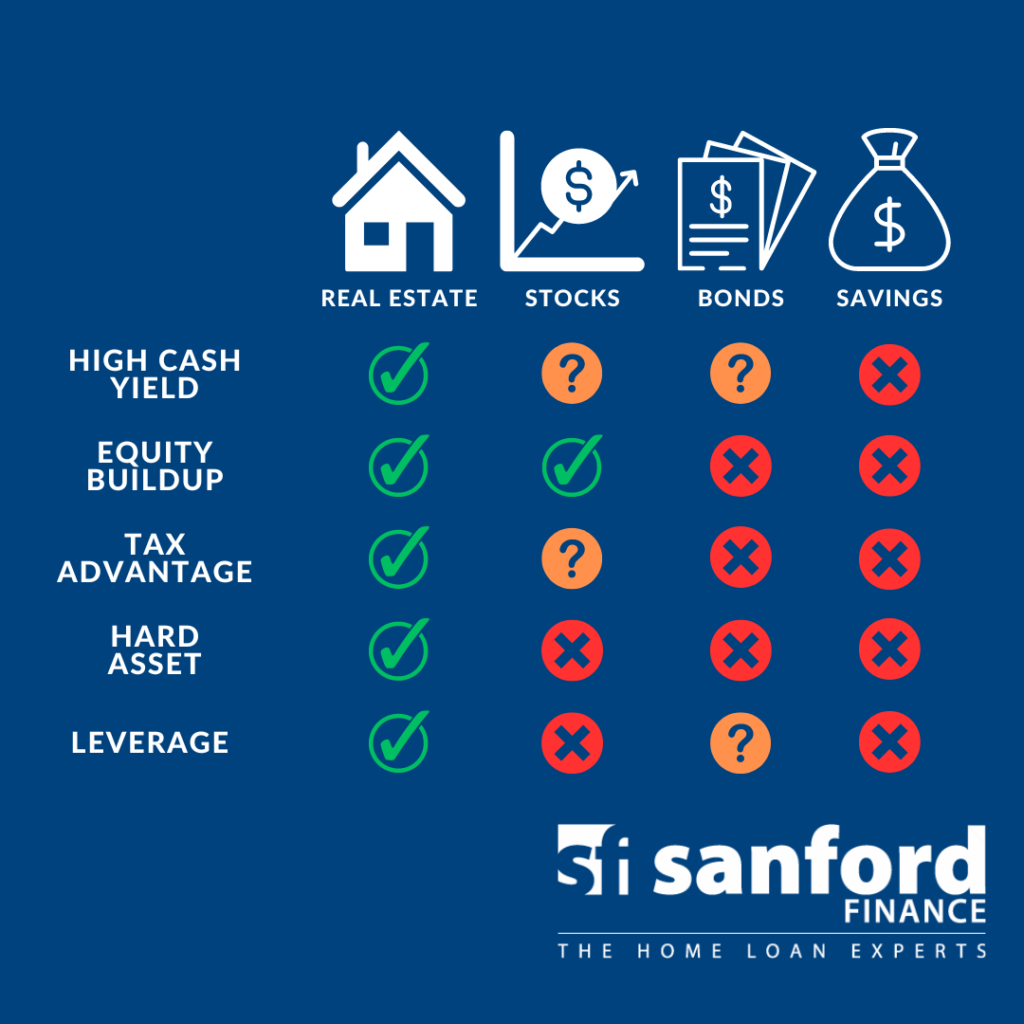

Thinking about investing in property? We can help

If you’re thinking about investing in property, our team are here to help. Together we’ll look at all the potential options, develop a strategy, secure finance and help you achieve your goals. Contact us today to get started.