Quick summary: 5% deposit. No Lenders Mortgage Insurance. No income cap. No place limit. Price caps vary by state — see the table and diagram below. If your suburb is under the cap, you likely qualify.

How the scheme works

The First Home Guarantee (FHBG) lets eligible first home buyers purchase a property with a 5% deposit and avoid paying Lenders Mortgage Insurance (LMI). The Australian Government guarantees up to 15% of the property’s value to your lender, bridging the gap to the usual 20% deposit threshold.

On a $1.5 million property in Sydney with a 5% deposit, the LMI saving alone can be $50,000 to $65,000. On a $950,000 property in Melbourne, the saving is typically $28,000 to $35,000. This is money that stays in your pocket — not added to your loan balance.

The scheme is administered by Housing Australia and delivered through a panel of participating lenders. You cannot apply directly to Housing Australia — applications are made through a participating lender or a mortgage broker like Sanford Finance who is accredited on that panel.

What changed from 1 October 2025

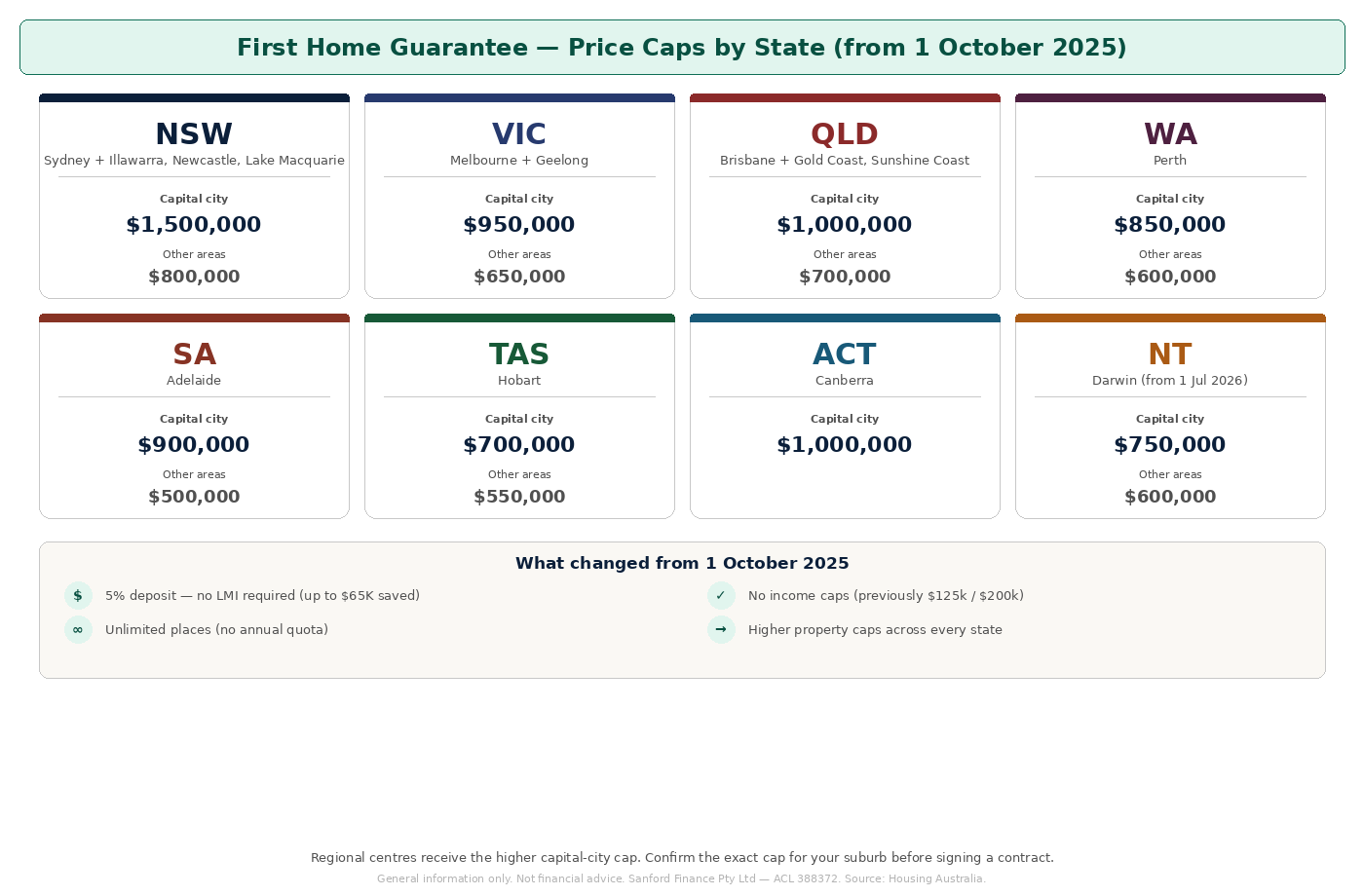

- Income caps removed: Previously $125,000 for singles and $200,000 for couples. Now removed entirely — the scheme is open regardless of income.

- Unlimited places: Previously capped at 10,000 places per year (later increased, but still finite). Now unlimited — every eligible applicant can access the scheme.

- Higher property price caps: Caps were lifted significantly across every state and territory to reflect current market values. Sydney jumped from $900,000 to $1,500,000 — a $600,000 increase that opens up virtually the entire Sydney market to first home buyers using the scheme.

- Regional scheme merged: The separate Regional First Home Buyer Guarantee (with its 12-month regional residency requirement) has been absorbed into the main FHBG. There is now one scheme for all eligible first home buyers regardless of where they buy.

Price caps by state and territory

The price caps apply to the property’s purchase price and its independently assessed value — both must be at or under the cap. The cap that applies is the one in force at the time of contract signing, based on the property’s location.

| State | Capital city + regional centres | Capital city cap | Other areas cap |

|---|---|---|---|

| NSW | Sydney, Illawarra, Newcastle, Lake Macquarie | $1,500,000 | $800,000 |

| VIC | Melbourne, Geelong | $950,000 | $650,000 |

| QLD | Brisbane, Gold Coast, Sunshine Coast | $1,000,000 | $700,000 |

| WA | Perth | $850,000 | $600,000 |

| SA | Adelaide | $900,000 | $500,000 |

| TAS | Hobart | $700,000 | $550,000 |

| ACT | Canberra | $1,000,000 | — |

| NT | Darwin (from 1 July 2026) | $750,000 | $600,000 |

First Home Guarantee price caps by state (from 1 October 2025)

Regional centres get the capital-city cap: Under the scheme, several regional centres receive the higher capital-city price cap: in NSW — Illawarra, Newcastle and Lake Macquarie; in Victoria — Geelong; in Queensland — the Gold Coast and Sunshine Coast. This is worth thousands in effective purchasing power. Confirm your suburb’s exact classification before signing anything — the boundary can split neighbouring streets.

Am I eligible?

The eligibility criteria are simpler than they used to be, but a few key requirements remain in place:

- Australian citizen or permanent resident, aged 18 or over.

- First home buyer, or someone who has not owned property in Australia in the past 10 years (the “fresh start” rule).

- Deposit between 5% and 20% of the property’s value — with genuine savings typically shown over 3 months.

- Owner-occupier purchase only — you must intend to live in the property. Investment purchases do not qualify.

- Purchase price under the cap for your specific suburb and postcode.

- Apply through a participating lender — there are over 30 lenders on the panel, including all major banks and many smaller lenders.

Combining schemes: how to stack the benefits

The First Home Guarantee is a federal scheme, and it can generally be combined with your state-based first home buyer concessions. This stacking is where the biggest wins are — and where a broker’s advice matters most. Some examples:

- Queensland — the $30,000 First Home Owner Grant on new builds (contracts before 30 June 2026) plus zero stamp duty on new homes (no price cap, effective 1 May 2025). Stack that on top of the FHBG and a first home buyer in Ipswich or Springfield can save $50,000 to $80,000 upfront on a new-build purchase.

- NSW — stamp duty relief on properties under $800,000, plus FHBG. First home buyers can combine both to purchase in Sydney’s growth corridors — including Leppington, Austral and Campbelltown — with meaningful concessional support.

- Victoria, WA, SA, TAS, ACT, NT — each state has its own first home owner grant and stamp duty concession structure. Some are exemptions; others are partial concessions. Your broker will map the right combination for your circumstances.

- Family Home Guarantee (2% deposit) — a separate federal scheme for single parents and single legal guardians with dependent children. If you qualify, you can access the scheme with a 2% deposit instead of 5%.

- First Home Super Saver Scheme — lets you make voluntary contributions to super and withdraw them tax-effectively for your deposit. Contributions and deemed earnings up to $50,000 total can be withdrawn.

Talk to Sanford Finance: Choosing which scheme to use — and which lender to apply through — makes a material difference to your final position. Not every lender is on the FHBG panel, and lender policies on genuine savings, HELP debt, gifted deposits and casual income all vary. We work with over 40 lenders and can map out the right combination of federal scheme, state concession and lender choice for your specific circumstances. Call (02) 9095 6888 or visit sanfordfinance.com.au to book a free consultation.

What to do next

- Check your eligibility — confirm you meet the criteria above and calculate your borrowing capacity.

- Confirm the price cap for your target suburb — the caps in this article are the headline figures; individual suburbs can have different classifications. Housing Australia has a postcode search tool at firsthomebuyers.gov.au.

- Get pre-approval — a pre-approved loan puts you in a stronger position when you find the right property. It also helps you understand what the lender will actually approve, versus what you might be able to borrow in theory.

- Speak to a mortgage broker — a broker on the FHBG panel can compare lenders, check your suburb’s cap, review your state concessions and structure the loan correctly from the outset.

Disclaimer: This article provides general information only and has been prepared without taking into account your objectives, financial situation or needs. Price caps, eligibility criteria and scheme rules are set by Housing Australia and may change. Always confirm the current position at firsthomebuyers.gov.au and seek professional advice before committing to a purchase. Sanford Finance Pty Limited — Australian Credit Licence 388372 — ABN 50 117 771 187.