Division 296 took effect on 1 July 2026, but a late redesign dropped its most controversial feature. Here’s where it landed and who it actually affects.

After nearly three years of debate, the Division 296 tax on large superannuation balances is now law and applies from the 2026-27 financial year. But the version that passed is materially different from the one that caused so much alarm. If you or your clients hold a total super balance approaching $3 million, this is worth reading closely.

The numbers that matter

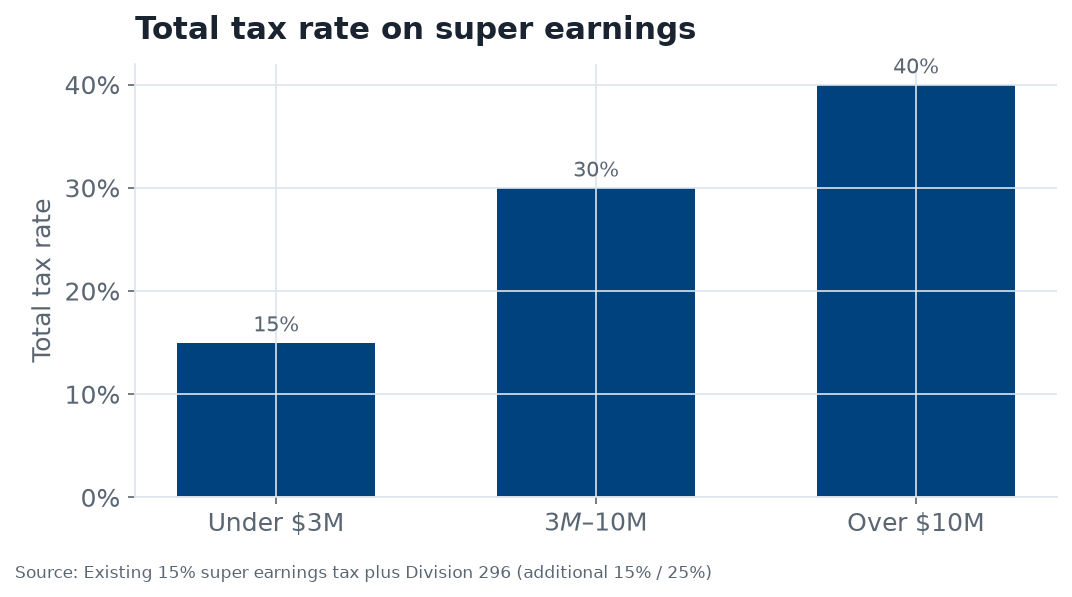

| $3MBalance threshold | 30%Total rate, $3–10M | 40%Total rate, over $10M | 1 Jul 2026Starts |

How the tax actually works

Division 296 sits on top of the existing 15% tax on super earnings. It imposes additional tax only on the proportion of a member’s earnings that relates to the portion of their Total Super Balance above the relevant threshold — not the whole balance. An extra 15% applies to earnings attributable to the slice between $3m and $10m, for a 30% total rate on that portion. Members with balances above $10m pay an additional 25% on earnings attributable to the balance above $10m, for a 40% total rate on that portion. Both thresholds are indexed to CPI, in $150,000 and $500,000 steps respectively.

Total tax rate on earnings, by balance tier

The additional tax is tiered, and the ATO calculates it from your Total Super Balance across all your funds — not separately for each fund. Earnings on the first $3 million keep the standard concessional rate.

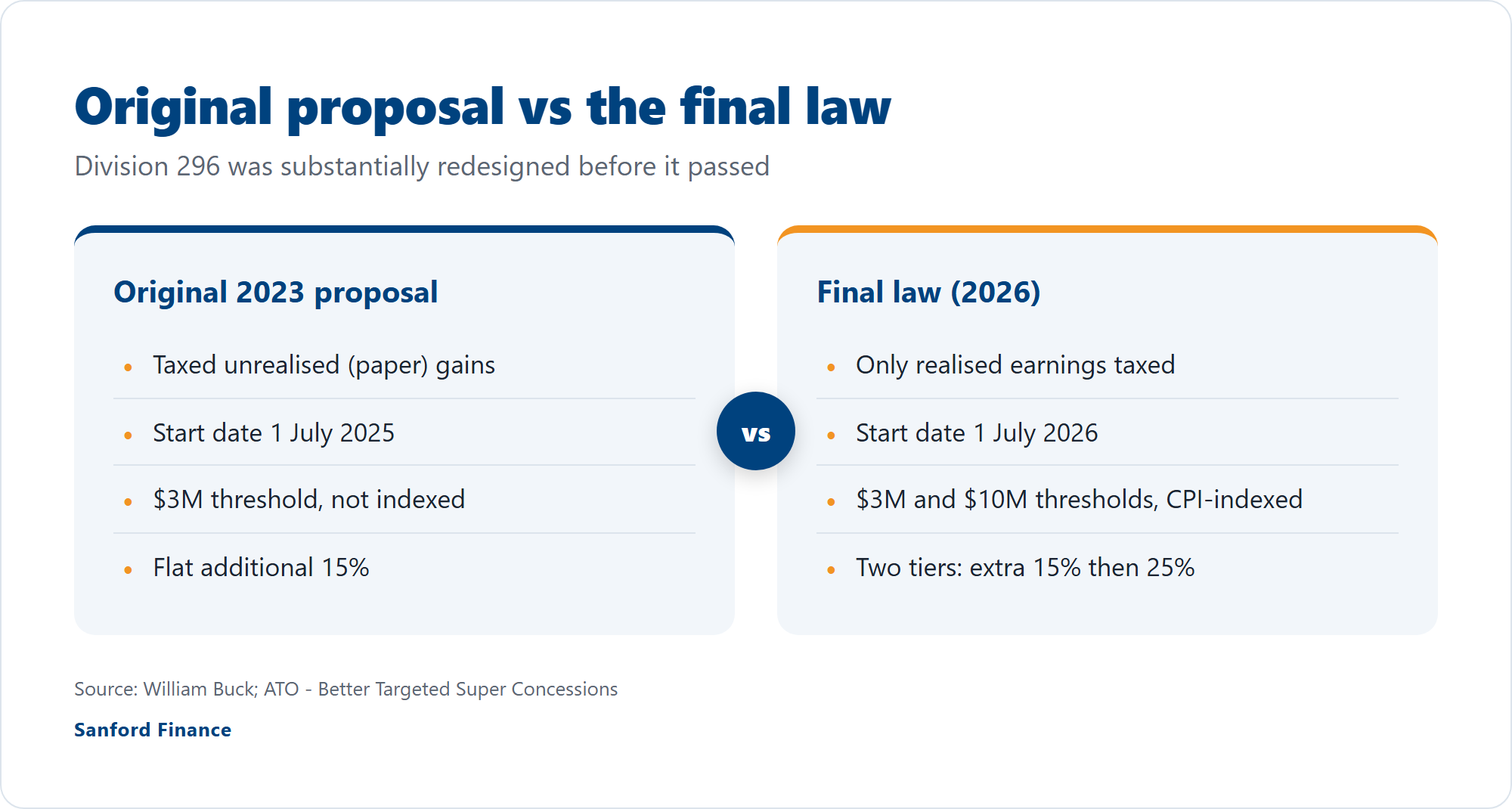

What changed between the draft and the law

The big reversal: no tax on unrealised gains

The original design would have taxed unrealised gains — paper increases in the value of assets you still hold. That drew heavy criticism, particularly for SMSFs holding property or farmland. The final law drops it entirely: only realised earnings — interest, dividends, rent and realised capital gains — are counted.

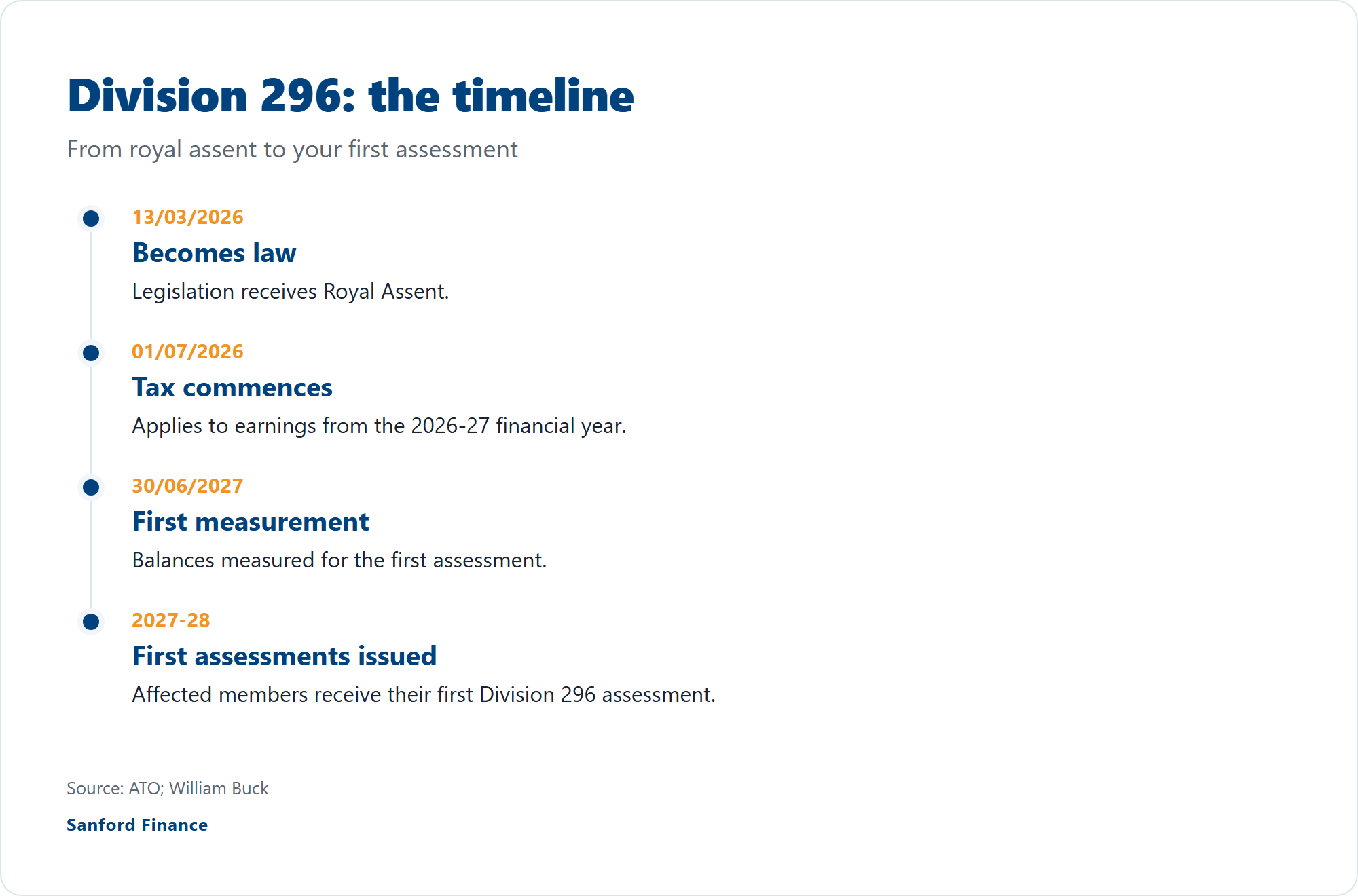

The dates to have in your diary

The first measurement date is 30 June 2027, with the first Division 296 assessments expected during the 2027–28 financial year.

What to think about now

There is no need to panic, but there is time to plan. Members approaching or exceeding the threshold may wish to review their contribution strategy, asset location and the timing of asset disposals with their financial adviser or tax professional. As always, the right answer depends on your circumstances — this is general information, not personal advice.

Could Division 296 affect you?

This information is general only and does not take into account your objectives, financial situation or needs. It is not credit assistance or personal advice. Consider whether it is appropriate for you and seek professional advice before acting. Sanford Finance Pty Ltd — Australian Credit Licence 388372.